The U.S. demand for solar panels reached approximately 40 GW in 2024 and is projected to grow to 50 GW annually by 2026, with an installed base already at 220 GW. Battery Energy Storage Systems (BESS) currently account for around 30 GW, but rapid growth is expected as intermittent solar generation and weaknesses in the U.S. energy grid drive adoption. Additional demand will also come from data centers, AI, and the electrification of transportation, with overall U.S. energy requirements forecasted to increase by at least 5% per year over the next decade.

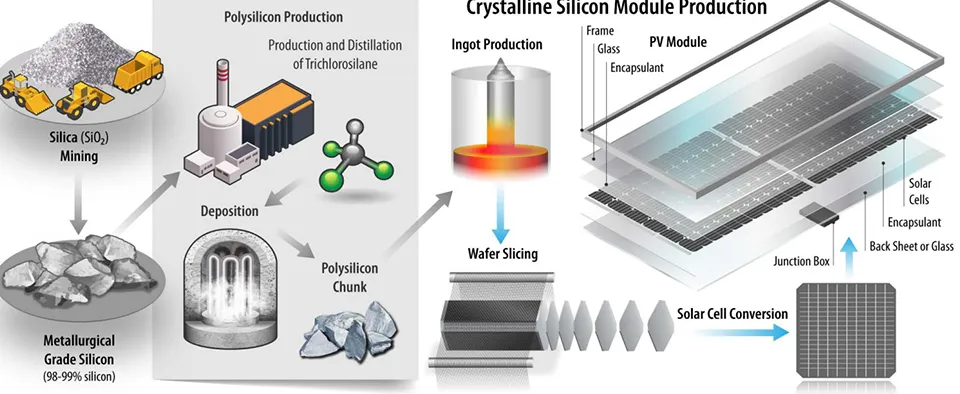

Today, more than 80% of the world’s solar panels and 70% of utility-scale BESS are manufactured in China or by Chinese producers. Chinese technology is recognized as the global standard in terms of efficiency, durability, and cost per watt, especially for solar panels. This has enabled Chinese firms to scale rapidly and dominate global supply chains.

Domestic producers, led by First Solar, can only meet about half of current demand. While U.S. production is expanding, Chinese companies are actively building facilities in America—initially simple module assembly plants and now moving toward more sophisticated cell manufacturing, battery assembly, and battery cell plants.

As of today, at least 23 U.S. facilities are operating with ten more in the pipeline, many partially or wholly owned by Chinese firms.

The U.S. regulatory framework remains uncertain but is shaping industry opportunities:

The combination of growing U.S. demand, limited domestic capacity, and excess manufacturing capacity in China has created a unique investment window. Chinese manufacturers, facing overcapacity and funding constraints, are increasingly open to partnerships with U.S. entities. This provides U.S. investors with opportunities to acquire majority stakes, secure technology transfer, and align with long-term U.S. energy policy goals.

Solar power is the cheapest and fastest-deployable energy source, with costs significantly lower than wind, coal, oil, or nuclear. Its continued expansion makes battery storage indispensable. Together, solar and BESS form the backbone of the global energy transition, and the United States represents the most critical growth market for the coming decade.